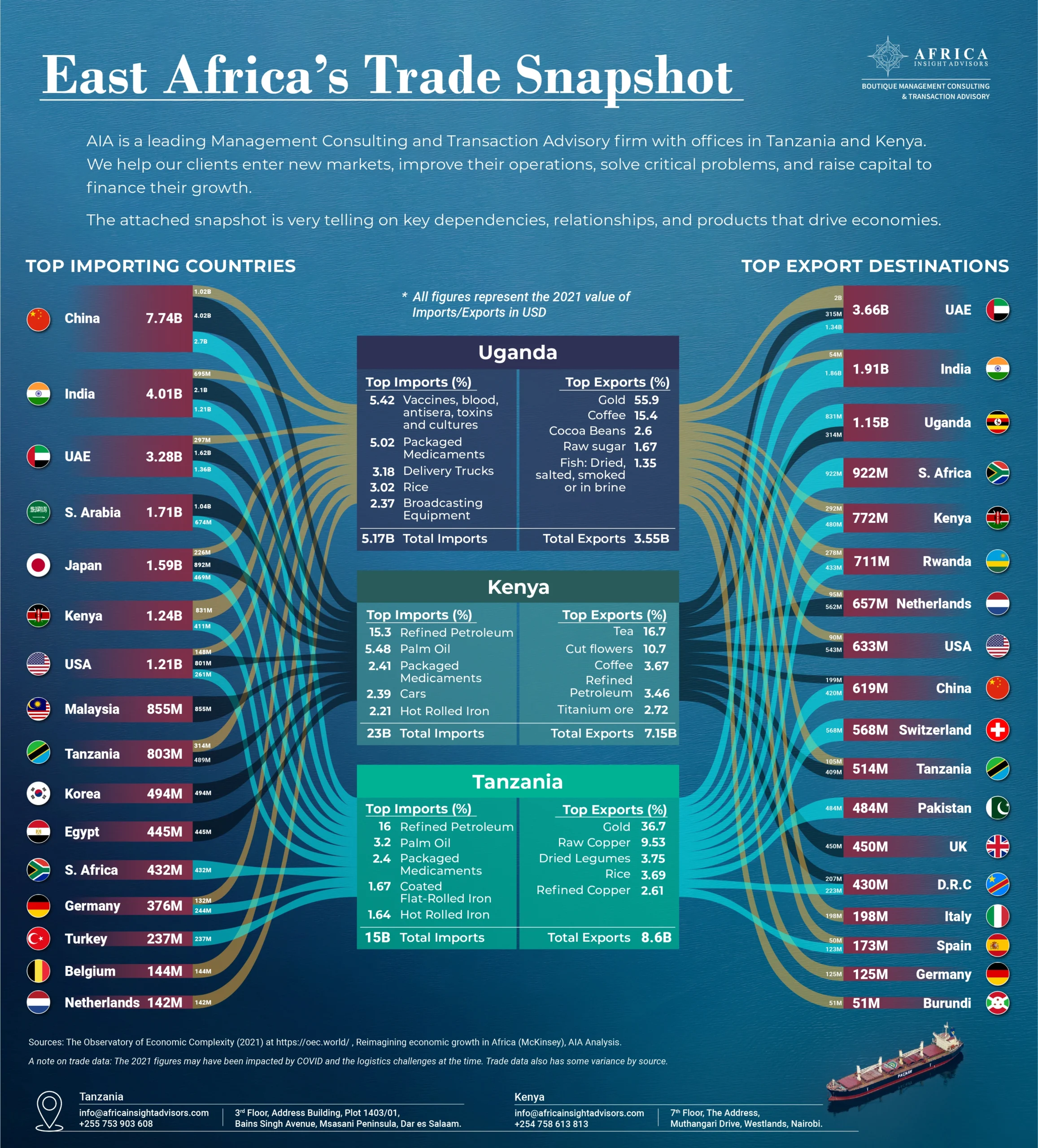

As can be seen on the snapshot, all of the countries have a trade deficit, with Kenya’s and Tanzania’s imports at 3x and 2x the value of exports, respectively.

How might this change in the years to come?

On the import side, let’s look at a few of the main products:

- With increasing urbanization, income growth, and infrastructure investments, passenger vehicles and motorbikes are more commonplace and achievable for the average citizen. Needless to say, refined petroleum imports are likely to grow for years to come.

- As we highlighted in another infographic earlier this year, construction in Tanzania is certainly on the upswing, not to mention large-scale infrastructure projects across the region (numerous power generation and transmission projects, EA Crude Oil Pipeline, standard gauge rail extensions, port upgrades and improvements, etc.). With a reliance on imported iron and steel, imports of these are also bound to increase in the years to come.

It is hard to see how exports could keep pace.

- Gold is a major export, but there hasn’t been a new large-scale (Special Mining License defined as CAPEX above $100m) mine constructed in Tanzania since 2012, so it is hard to see these figures growing rapidly unless the gold price climbs dramatically.

- There are a wide variety of agricultural crops exported, but the sector is plagued by a host of challenges that mean rapid growth is unlikely:

- Below world average yields across most value chains.

- The increasing impact of climate change and unpredictable weather on yields.

- Challenges to access and utilize inputs (fertilizer, improved seed varieties, etc.) and mechanization (tractors, processing equipment, etc.) and infrastructure limitations which impact the movement and storage of agriproducts.

A trade deficit is neither inherently good nor bad, but in the case of East Africa, there are certainly implications.

Kenya has significant foreign denominated debt levels in particular, the USD2.7b Eurobond that is due to mature in mid-2024. Recently, the President of Kenya stated that 60% of tax revenues go to making debt repayments (https://africacheck.org/fact-checks/reports/kenyan-president-william-ruto-right-nearly-60-countrys-tax-revenue-goes). Further currency weakening will have a compounding negative effect on the country’s prospects.

The Tanzanian shilling has already devalued by roughly 10% this year to a stated 2550TZS to the dollar, and there has been quite a bit of recent press on the shortage of USD in Tanzania. As with trade deficits, a currency devaluation is neither inherently good nor bad, but a rapid devaluation can have catastrophic implications for countries and companies.

With the obvious caveat, as previously mentioned, that a trade deficit isn’t necessarily a negative, it is clear why the governments of Tanzania and Kenya, and perhaps Uganda as well, would want to keep an eye on the balance of trade. To state a painfully obvious conclusion, reliance on imports is only set to increase as the economies grow and develop. To keep exports roughly in line, it is then essential for governments to do everything they can to incentivize FDI that focuses on local value addition, and bring in players who have the ability to massively develop sectors and value chains.