We are working on a few exciting projects in the construction material space, and this infographic perfectly captures the raw potential of the sector.

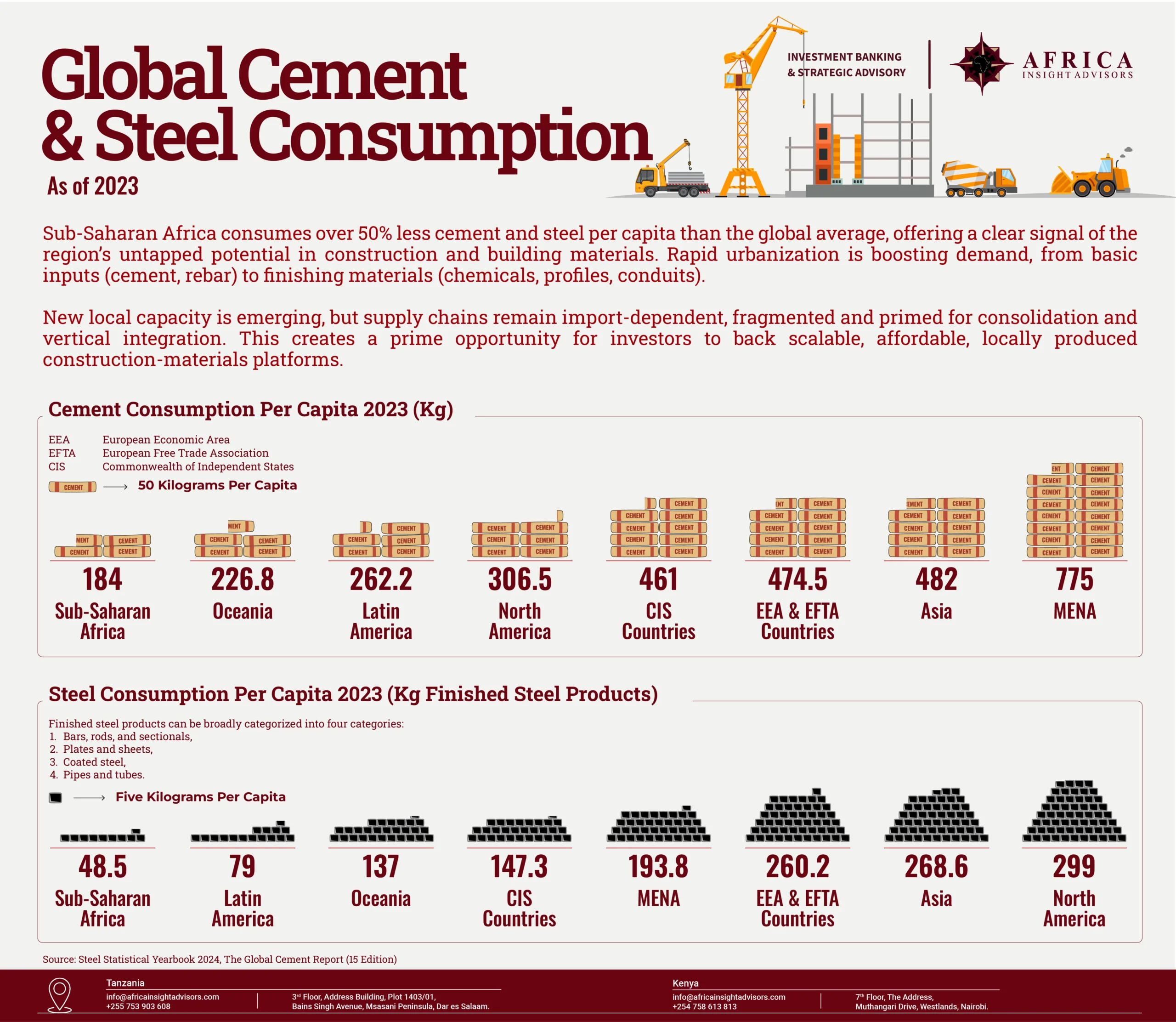

Sub-Saharan Africa consumes over 50% less cement and steel than the global averages—offering a clear signal of the region’s untapped potential in construction and building materials. These figures serve as proxies for a much broader opportunity: from concrete and rebar to finishing inputs like construction chemicals, aluminum profiles, and electrical conduits. As urban populations grow and the need for housing and infrastructure surges, SSA stands out as one of the world’s most compelling frontiers for construction sector growth.

The focus in affordable housing, commercial and retail developments, and critical infrastructure like roads, ports, and energy is beginning to translate into new capacity investments—from cement plants in Nigeria and Ethiopia to expanded distribution and warehousing capabilities in fast-growing cities. And yet, much of the value chain remains import-dependent, fragmented, and ripe for consolidation, modernization, and vertical integration.

For private equity and strategic investors, this is a prime opportunity to back scalable platforms across the construction value chain. The shift from import substitution to localized production and value addition is not only underway—it’s accelerating. We see real potential in raising capital for businesses that can deliver affordable, high-quality materials at scale and help shape the next generation of Africa’s built environment.

For more updates on what we do, connect with us on LinkedIn.

Looking to explore investment opportunities in Africa’s construction materials sector? Let’s have a chat.