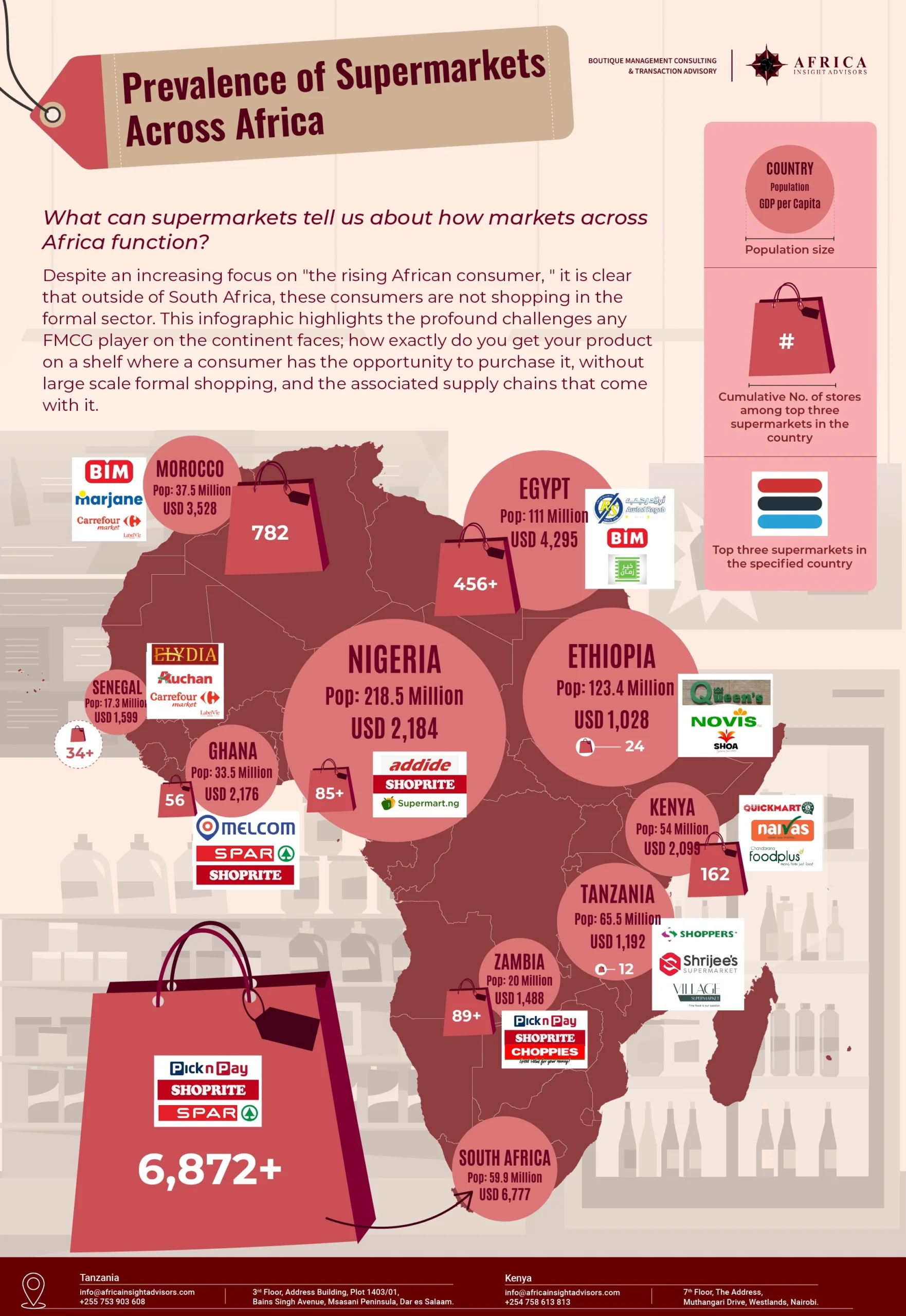

While supermarket chains are ubiquitous worldwide, they have yet to firmly take root in most African countries. The size and number of supermarkets are a clear indicator of market formality, and this infographic highlights that the informal market is still king across the continent (with the exception of South Africa).

Many have documented The last mile challenge well, but the bigger question is: how should FMCG players tackle this problem?

Over the years, we have executed numerous engagements to help clients enter new markets and ultimately push products all the way to informal market shelves. For our market entry work, there are generally three distinct phases.

- Market Assessment: Feasibility studies, competitor assessments, regulatory analysis, market sizing, etc., to gather the facts and figures to make an informed go-or-no-go market entry decision.

- Strategy Development: Further data collection (i.e., consumer perceptions) and planning on how to actually execute in the market, given local nuance.

- Execution/Launch: Kickoff and implementation of phase two plans.

The last mile problem commonly comes up in phase two. Companies like the market, and are confident there is demand for their product. However, they are still determining how to get it to the last mile. While a client determines the exact scope of work, here is how we start trying to break down this problem:

- Geographic focus: Where the product will be sold given socio-economic factors, competitor presence, demand dynamics, and other factors that may help narrow down where sales will occur.

- Identify the last mile sales channel: What kind of shops sell the product type in question in the target geographic areas? General shops/Dukas or speciality stores (i.e., hardware, home goods, or beauty).

- Route to market: How are informal retailers serviced in the relevant product space—wholesalers, distributors, etc?

This boots-on-the-ground engagement helps narrow the focus and identify third-party companies active in the space that could potentially be engaged to carry an additional product, but no one player is going to give full market penetration. Realistically, given the vast number of outlets that need servicing in informal markets, many FMCG players use a combination of in-house distribution, wholesalers, and third-party distributors.

The last mile problem is a solvable problem, but it doesn’t happen overnight. On-the-ground data collection guides initial market entry, and over time, FMCG players can refine their approach to increase their penetration and presence.

Connect with us on LinkedIn for more on-the-go insights.